The Iowa Public Employees' Retirement System (IPERS) is a vital cornerstone for the financial security of public employees in Iowa. With over six decades of service to its members, IPERS provides a dependable and comprehensive retirement program for employees across a variety of public sectors. Whether you're a teacher, firefighter, or state government employee, understanding how IPERS Iowa works is essential to securing your financial future.

IPERS Iowa serves more than 375,000 members, including active, retired, and inactive employees. The system is designed to ensure that public employees have access to a stable income after their working years. Notably, IPERS stands apart from typical retirement savings plans by offering defined benefits, which means your retirement income is calculated based on a formula rather than being directly tied to investment returns. This guarantees a predictable and steady income stream for retirees.

In this article, we dive deep into the structure, benefits, and eligibility requirements of IPERS Iowa. From understanding how contributions are made to exploring whether you qualify, we’ve got everything covered. Whether you’re a current member, someone planning to join, or simply curious about this system, this guide is tailored to provide you with comprehensive and actionable insights.

Read also:Revitalizing Your Skin With Virgin Coconut Oil Benefits And Uses

Table of Contents

- What is IPERS Iowa?

- Who Qualifies for IPERS Iowa Benefits?

- How Does IPERS Iowa Work?

- IPERS Iowa Benefit Plan

- How to Calculate Your IPERS Benefits?

- IPERS Iowa Contribution Rates

- Is IPERS Iowa a Good Retirement Plan?

- What Happens If I Leave My Job?

- Can You Withdraw Funds Early from IPERS Iowa?

- Is IPERS Iowa Taxable?

- How Do I Enroll in IPERS Iowa?

- Common Misconceptions About IPERS Iowa

- Frequently Asked Questions

- Conclusion

What is IPERS Iowa?

The Iowa Public Employees' Retirement System (IPERS) is a state-administered retirement program established in 1953. It offers defined benefit plans to eligible public employees in Iowa, ensuring financial stability during retirement. Unlike 401(k)-type plans, IPERS provides predictable monthly benefits based on a formula that includes factors like years of service, age, and average salary. This system is backed by employer and employee contributions, as well as investment returns, making it a robust and reliable retirement option.

Key Features of IPERS Iowa

- Defined benefit retirement plan offering predictable monthly payments

- Covers a wide range of public employees, including teachers, police officers, and government workers

- Funded through a combination of contributions from both employees and employers

- Oversees over $40 billion in assets, ensuring long-term sustainability

Why Is IPERS Important?

IPERS plays a crucial role in providing financial security for Iowa’s public employees. With the rising cost of living and uncertainties in the stock market, having a guaranteed source of income post-retirement is invaluable. Moreover, IPERS ensures that retirees remain financially independent, reducing their reliance on state or federal assistance programs.

Who Qualifies for IPERS Iowa Benefits?

To qualify for IPERS Iowa, you must be a public employee working for an eligible employer in Iowa. This includes state and local government agencies, public schools, and other qualifying organizations. However, not all employees automatically qualify; certain groups like contractors and temporary workers may not be eligible.

Eligibility Criteria

Here are the essential eligibility requirements for IPERS Iowa:

- Must be employed by a covered employer

- Part-time and full-time employees are eligible

- Temporary employees may qualify under certain conditions

- Independent contractors are excluded

Who Are the Covered Employers?

Covered employers include a wide array of public-sector organizations such as:

- State government entities

- Public school districts

- Municipal governments

- Public universities and colleges

How Does IPERS Iowa Work?

IPERS operates as a defined benefit plan, which means your retirement benefits are calculated based on a specific formula rather than market performance. This formula takes into account your years of service, age at retirement, and average salary over your highest-earning years. Both employees and employers contribute a percentage of your salary to the system, which is then invested to grow the fund.

Read also:Affordable Used Pc For Sale Your Comprehensive Guide To Making The Right Choice

Contribution Breakdown

Here’s how contributions are structured:

- Employees contribute a fixed percentage of their salary

- Employers match or exceed the employee contribution

- Contributions are invested in a diversified portfolio to ensure growth

Defined Benefit vs. Defined Contribution Plans

Unlike defined contribution plans like a 401(k), IPERS guarantees a steady income after retirement. This makes it an attractive option for those seeking financial predictability. While defined contribution plans rely on investment performance, defined benefit plans like IPERS provide a safety net against market volatility.

IPERS Iowa Benefit Plan

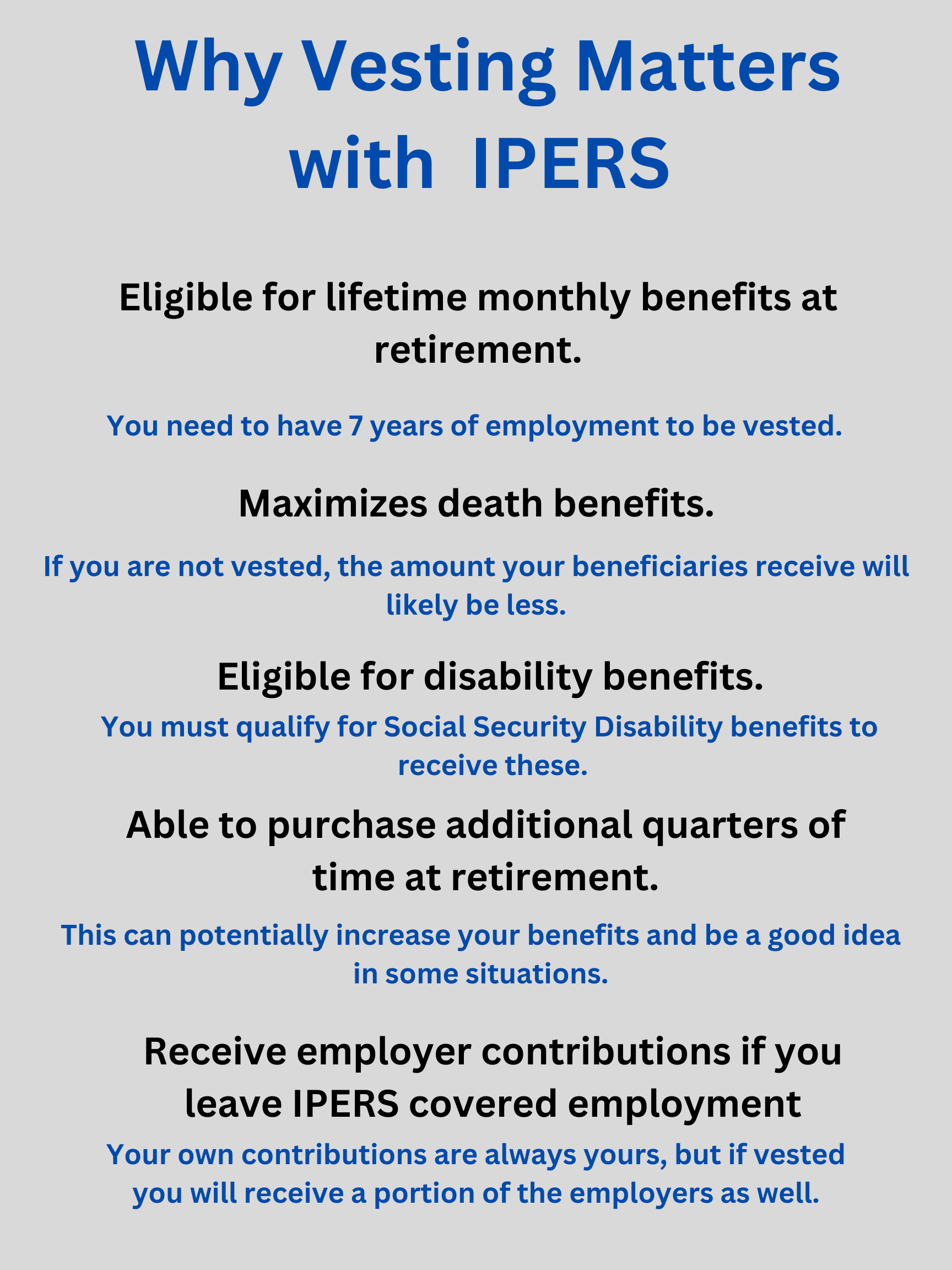

The IPERS benefit plan offers numerous features designed to ensure financial security for its members. Key highlights include lifetime monthly payments, survivor benefits, and disability provisions. The plan is structured to adapt to the diverse needs of its members, ensuring that everyone receives the support they need.

Types of Benefits

Here are the main types of benefits offered by IPERS:

- Retirement benefits

- Disability benefits

- Survivor benefits

Additional Perks

In addition to the core benefits, IPERS members enjoy other advantages such as:

- Cost-of-living adjustments

- Access to financial planning resources

- Flexibility in retirement age and payout options

How to Calculate Your IPERS Benefits?

Calculating your IPERS benefits involves a straightforward formula that considers your years of service, final average salary, and a multiplier based on your employment tier. The formula ensures that long-term employees receive higher benefits, rewarding loyalty and tenure.

Benefit Calculation Formula

The basic formula is:

Final Average Salary x Multiplier x Years of Service = Annual Benefit

For example, if your final average salary is $50,000, your multiplier is 2%, and you have 30 years of service, your annual benefit would be:

$50,000 x 0.02 x 30 = $30,000 per year

Factors Affecting Your Benefits

Your benefits may vary based on:

- Age at the time of retirement

- Employment tier (Regular, Special Service, etc.)

- Cost-of-living adjustments

IPERS Iowa Contribution Rates

IPERS contribution rates are reviewed annually and are subject to change based on the system’s financial health. Both employees and employers contribute to the fund, ensuring its long-term sustainability.

Current Contribution Rates

As of 2023, the contribution rates are:

- Regular Members: 6.29% (employee), 9.44% (employer)

- Special Service Members: Rates vary based on specific job roles

Why Are Contributions Important?

Contributions form the backbone of the IPERS fund, ensuring that benefits are adequately funded for current and future retirees. Regular reviews and adjustments help maintain the system’s fiscal health, providing peace of mind to its members.

Is IPERS Iowa a Good Retirement Plan?

Absolutely. IPERS Iowa is widely regarded as one of the most reliable retirement plans in the United States. Its defined benefit structure, coupled with robust funding and management, makes it an excellent choice for public employees seeking financial stability in retirement.

Strengths of IPERS

- Predictable income post-retirement

- Cost-of-living adjustments

- Strong financial oversight

Potential Drawbacks

While IPERS offers numerous advantages, it may not be ideal for everyone. For instance, employees who leave public service early may not fully benefit from the system. Additionally, the lack of portability compared to defined contribution plans can be a limitation for some.

Frequently Asked Questions

- What is the minimum retirement age for IPERS? The minimum retirement age is generally 55, but it may vary based on your employment tier and years of service.

- Can I transfer my IPERS benefits if I move out of state? While you can receive your benefits anywhere, the contributions themselves cannot be transferred to another retirement system.

- Are IPERS benefits taxable? Yes, IPERS benefits are subject to federal income tax and may also be taxable at the state level, depending on your location.

- Can I withdraw my contributions if I leave my job? Yes, you can withdraw your contributions, but doing so forfeits your eligibility for future benefits.

- How is the IPERS fund managed? The IPERS fund is managed by a professional investment team under the oversight of a board of trustees.

- Does IPERS offer disability benefits? Yes, IPERS provides disability benefits for members who meet specific criteria.

Conclusion

IPERS Iowa is more than just a retirement plan; it’s a promise of financial security for public employees. With its defined benefit structure, robust funding, and comprehensive coverage, IPERS stands out as a reliable and efficient system. Whether you’re already a member or considering joining, understanding IPERS is crucial for making informed decisions about your financial future.

For more detailed information, you can visit the official IPERS website.